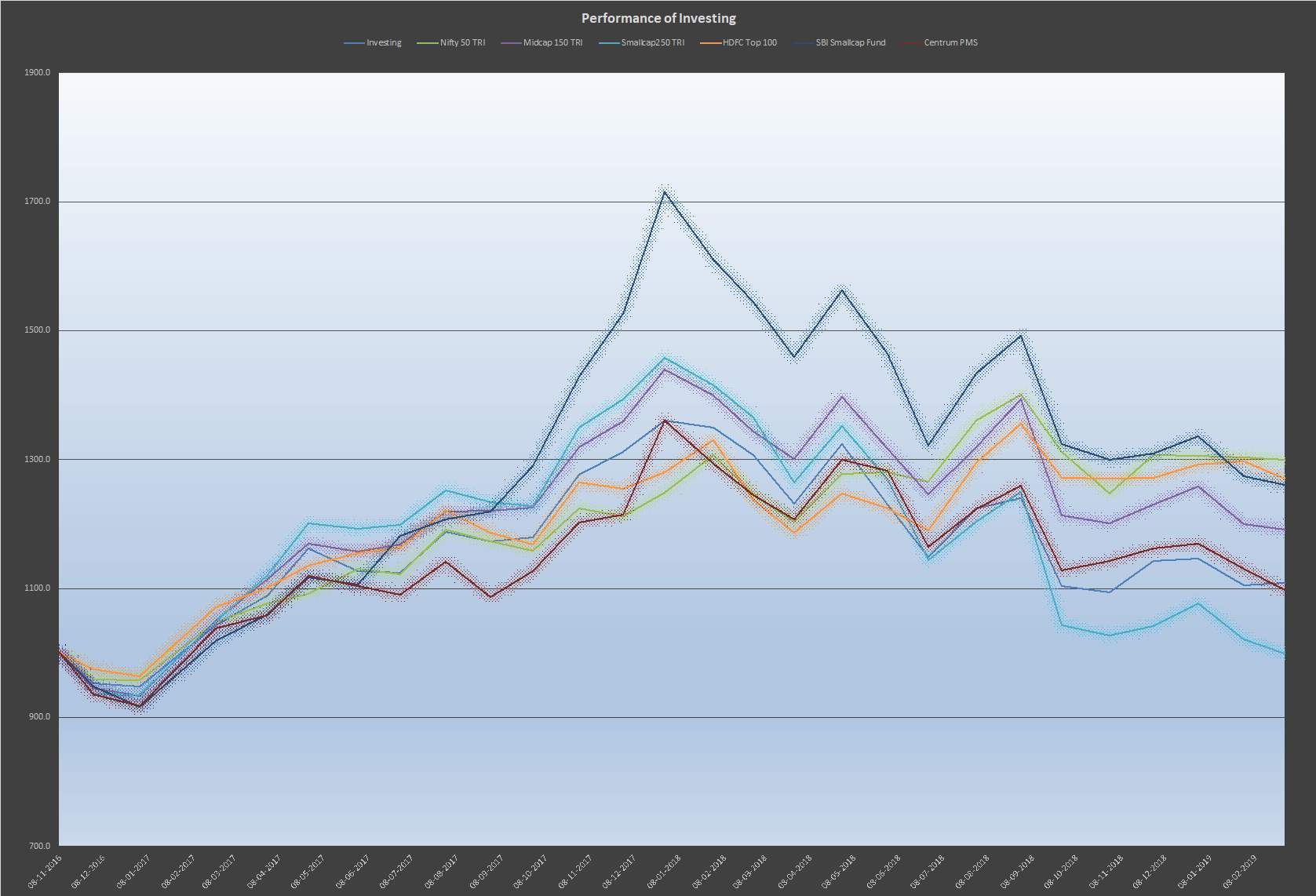

That momentum influences stock prices is well known since a long time. Two Centuries of Momentum is an article which summarizes the evidence of momentum in financial markets since the last 200 years. It also gives a behavioural basis and an information theory basis for the prevalence of momentum, and thus extends the purist approach to momentum being a ‘risk factor’ for which a risk premium should exist in the form of superior returns.

Momentum is simply a restatement, in financial market terms, of Newton’s First Law of Motion. Prices which have risen a lot, tend to keep rising, and prices which have fallen a lot, tend to keep falling.

There are hundreds of studies in the academic literature to show that momentum works. Even if we see the records of many successful investors, you can find that they often choose stocks which have high momentum, and their buying propels them even more.

How can you measure momentum in stock prices? Well there are many ways to do so. One of the simplest approaches is to measure returns over a lookback period, typically 12 months, rank the stocks in the investing universe on these 12 month returns, and then buy the top quintile (or buy the top quintile and short the bottom quintile). By top quintile, I mean the top 10% of stocks in the investing universe. When we mean ‘investing universe’. it is usually related to a benchmark, like an index. So you take all the stocks in an index, and buy the top 10%.

What about allocation of stocks within this top 10%, or top 5%? There are many weighting schemes possible, but the two most common ones are equal weighted and factor weighted. This is best explained by an example. Suppose you take the NSE50 as the benchmark, and rank all 50 stocks by the returns over the past 365 days (the ‘Look Back Period’). Suppose you now choose the top 10% of stocks (i.e., the top 5 stocks). If you wish to invest 10 lakhs at this time, one option is to allot 2 lakhs towards buying each of the 5 stocks. This is equal weighting. Factor weighting involves alloting more than 2 lakhs to the highest ranked stock, and less than 2 lakhs to the lowest ranked stock of the 5 stocks. That is, factor weighting gives more allocation to higher ranked stocks than to lower ranked stocks and equal weighting gives the same allocation to all the selected stocks.

There are many ways to measure momentum. One is to simply rank the stocks on their returns of the last 365 days. Another way is a variation of this. At the end of the 12 month, you rank stocks on their returns after 11 months, and give a rest period of 1 month. This is based on the idea that momentum typically flags after 11 months, before resuming.

A third way to measure momentum is to to examine the distance between the stock price and a long period moving average (say the 200 period moving average).

A fourth way to measure momentum is to look at what a call Alpha Momentum. Recall our discussion in the previous post on the CAPM, where we said that stock prices move because of the market factor. In other words, this can be expressed as

Return of the stock=A+B(Return of the Market-Risk Free Rate)+C

A is known as Alpha, B is Beta and C is a noise term. Beta signifies how much the stock moves with the market. If Beta is small (i.e., less than 1), than the stock price will move less than the index movement. If Beta is large, small market movements will cause large changes in the stock price.

Alpha is idiosyncratic. Both Alpha and Beta are typical of the stock in question. High Alpha means that a large part of the stock movement is not explained by the market factor alone. Low Alpha means that the stock moves more or less in line with the market. If the market rises, it rises, and if the market falls, the stock falls too.

So Alpha is a sort of idiosyncratic momentum term, and we can rank stocks in terms of Alpha as well. This turns out to be a very potent way of measuring momentum, as we will see.